When selling puts, such as we do in our Steady Momentum PutWrite strategy, there are many questions a trader must answer: What expiration should I use? What strike should I sell? Should I choose that strike based on delta or percentage out of the money?

Should I place all my contracts at one strike and expiration, or split it up for diversification? Should I wait until expiration as my natural exit, or roll early? Should I handle winning trades the same way as losing trades? Should I only sell enough contracts to be fully cash secured, or use leverage?

In this article, I’m going to address the question of choosing strikes based on delta, while keeping the other variables constant, in order to show some historical performance comparisons of SPX put options from 2001-2018. Whenever I make trading decisions, I always remind myself of a couple quotes from W.E. Deming…

“In God we trust, all others must bring data.”

“Without data you’re just another person with an opinion.”

Assumptions held constant for the following backtests…

- Product: SPX

- Period: 2001-2018

- Entry: 30 DTE

- Exit: 80% of credit received, or 5 DTE, whichever comes first

- Position Sizing: 100% notional/cash secured (no leverage)

- Collateral yield: 0%

- Commissions and slippage: Not included

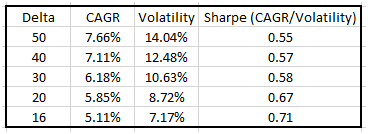

Based on those assumptions, here’s the data for trades placed at different deltas.

- Higher risk has historically resulted in higher reward…As strikes move away from at the money (ATM), volatility and annualized returns both decline. This is what we would have expected to see in a world of not perfectly, but highly efficient markets.

- Sharpe Ratio’s increased with out of the money (OTM) options. This is what I find most interesting and worthy of further discussion.

Why would there be higher Sharpe Ratio’s with out of the money options, and is there any opportunity based on this data? Research from AQR has come to similar conclusions that Sharpe Ratios tend to increase the further out of the money an option is sold. This might be for the same reason that we see a linear decrease in historical Sharpe Ratios for US treasuries the further out on the yield curve you go (i.e., comparing Sharpe Ratios of 1/2/5/10/30-year treasuries): Aversion to and/or constraints against the use of leverage.

If you’re an investor who is unwilling or unable to use leverage, your only choice to maximize expected returns is to sell the riskiest option (ATM) and buy the riskiest treasury bond (30-year). This being a common theme among market participants can create market forces that impact prices. But if you are willing and/or able to use leverage, you could simply lever up OTM put options or shorter-term treasury futures to your desired risk level, and get paid more per dollar risked. Isn’t that the objective…the most gain with the least pain?

Of course, risk cannot be eliminated…only transformed, and leverage creates risks of its own and should be used responsibly. Unfortunately, it too often isn’t. As I wrote in a recent article, excessive leverage is the number one mistake I see retail and even occasionally “professional” investors make. In our Steady Momentum strategy, we sell OTM puts and lever up to around 125% notional to give us a similar expected return as ATM puts with slightly less volatility. We also collateralize our contracts with short and intermediate term bonds instead of cash, as collateral ends up being a significant portion of total returns with put selling strategies.

Jesse Blom is a licensed investment advisor and Vice President ofLorintine Capital, LP. He provides investment advice to clients all over the United States and around the world. Jesse has been in financial services since 2008 and is aCERTIFIED FINANCIAL PLANNER™professional. Working with a CFP® professional represents the highest standard of financial planning advice. Jesse has a Bachelor of Science in Finance from Oral Roberts University. Jesse manages theSteady Momentumservice, and regularly incorporates options into client portfolios.

What Is SteadyOptions?

Full Trading Plan

Complete Portfolio Approach

Diversified Options Strategies

Exclusive Community Forum

Steady And Consistent Gains

High Quality Education

Risk Management, Portfolio Size

Performance based on real fills

Non-directional Options Strategies

10-15 trade Ideas Per Month

Targets 5-7% Monthly Net Return

Recent Articles

Articles

Pricing Models and Volatility Problems

Most traders are aware of the volatility-related problem with the best-known option pricing model, Black-Scholes. The assumption under this model is that volatility remains constant over the entire remaining life of the option.

By Michael C. Thomsett, August 16

- Added byMichael C. Thomsett

- August 16

Option Arbitrage Risks

Options traders dealing in arbitrage might not appreciate the forms of risk they face. The typical arbitrage position is found in synthetic long or short stock. In these positions, the combined options act exactly like the underlying. This creates the arbitrage.

By Michael C. Thomsett, August 7

- Added byMichael C. Thomsett

- August 7

Why Haven't You Started Investing Yet?

You are probably aware that investment opportunities are great for building wealth. Whether you opt for stocks and shares, precious metals, forex trading, or something else besides, you could afford yourself financial freedom. But if you haven't dipped your toes into the world of investing yet, we have to ask ourselves why.

By Kim, August 7

- Added byKim

- August 7

Historical Drawdowns for Global Equity Portfolios

Globally diversified equity portfolios typically hold thousands of stocks across dozens of countries. This degree of diversification minimizes the risk of a single company, country, or sector. Because of this diversification, investors should be cautious about confusing temporary declines with permanent loss of capital like with single stocks.

By Jesse, August 6

- Added byJesse

- August 6

Types of Volatility

Are most options traders aware of five different types of volatility? Probably not. Most only deal with two types, historical and implied. All five types (historical, implied, future, forecast and seasonal), deserve some explanation and study.

By Michael C. Thomsett, August 1

- Added byMichael C. Thomsett

- August 1

The Performance Gap Between Large Growth and Small Value Stocks

Academic research suggests there are differences in expected returns among stocks over the long-term. Small companies with low fundamental valuations (Small Cap Value) have higher expected returns than big companies with high valuations (Large Cap Growth).

By Jesse, July 21

- Added byJesse

- July 21

How New Traders Can Use Trade Psychology To Succeed

People have been trying to figure out just what makes humans tick for hundreds of years. In some respects, we’ve come a long way, in others, we’ve barely scratched the surface. Like it or not, many industries take advantage of this knowledge to influence our behaviour and buying patterns.

- Added byKim

- July 21

A Reliable Reversal Signal

Options traders struggle constantly with the quest for reliable

By Michael C. Thomsett, July 20

- Added byMichael C. Thomsett

- July 20

Premium at Risk

Should options traders consider “premium at risk” when entering strategies? Most traders focus on calculated maximum profit or loss and breakeven price levels. But inefficiencies in option behavior, especially when close to expiration, make these basic calculations limited in value, and at times misleading.

By Michael C. Thomsett, July 13

- Added byMichael C. Thomsett

- July 13

Diversified Leveraged Anchor Performance

In our continued efforts to improve the Anchor strategy, in April of this year we began tracking a Diversified Leveraged Anchor strategy, under the theory that, over time, a diversified portfolio performs better than an undiversified portfolio in numerous metrics. Not only does overall performance tend to increase, but volatility and drawdowns tend to decrease: